THE GREAT INVISIBILITY: How French Companies Are Disappearing from the AI Economy

Key Takeaways (In Brief)

Featured in Les Echos: Read the full article

Our study, "The Great Invisibility: How French Companies Are Disappearing from the AI Economy," assesses the economic consequences of the lack of visibility in LLMs (conversational AI agents like ChatGPT) for French companies. It is a statistical approach based on 857 queries on 3 LLMs (ChatGPT, Perplexity, Mistral LeChat) on a test sample of 20 French economic leaders.

Key Figures:

- Artificial Invisibility Index of 27 points - French champions do not even appear in the response in more than a quarter of cases;

- Artificial Downgrade Index of 16 points – French champions are less often recommended as the 1st choice by AIs and experience a downgrade compared to their actual leadership.

- €6 Billion: The economic cost of AI invisibility suffered in 2026 by these 20 French champions.

Main Lessons:

- Strong disparity in results between B2C and B2B companies: B2C leaders are less penalized, while some B2B leaders are completely invisible.

- "Linguistic Ghetto" Bias: For the same queries, French companies are more invisibilized and downgraded when the query language is English. This creates a "linguistic ghetto" phenomenon, curbing the ability of French champions to conquer new markets.

- Significant risk of stalling for French companies: In 2025, AI searches represented 10% of global search traffic; they will represent 30% in 2026 and 50% in 2028. Being invisible in AI responses could significantly degrade the ability of French companies to acquire new customers and endanger their economic model.

French companies do not suffer from a deficit of technical skills or innovation, but from a deficit of semantic translation of these skills into the formats and channels favored by language models. A rapid investment by French companies in GEO (the set of techniques aimed at optimizing the presence of an entity in responses generated by LLMs) would allow them to correct their AI visibility deficit.

If French companies lag several years behind in implementing GEO strategies, they could find themselves permanently confined to their domestic or regional markets, while their American and Chinese competitors capture the bulk of global growth via their superior algorithmic visibility. Invisibility in AI would then no longer be a simple marketing problem, but a structuring factor of 21st-century geo-economics.

Introduction: The New Battlefield

The digital economy is undergoing a silent but decisive mutation. According to SimilarWeb and Semrush data consolidated in the fourth quarter of 2025, traffic to artificial intelligence conversational interfaces has grown by 527% in twelve months, while organic traffic to traditional search engines recorded its first structural decline since the creation of Google. This inversion is not cyclical: projections place the tipping point — the moment when traffic to Large Language Models (LLMs) will exceed that to classic search engines — before the end of 2028.

This shift completely redefines commercial discovery mechanisms. In the traditional search economy, being absent from the first page of Google was a major competitive handicap; in the emerging generative AI economy, not being cited by ChatGPT, Perplexity, or Gemini equates to pure and simple invisibilization. The difference is fundamental: where search engines present ten results among which the user makes a selection, generative models produce a single response synthesizing a limited number of sources and their training data. The challenge is no longer to be referenced, but to be recommended. It is no longer "being on Google" that counts, it is "being cited by AI".

However, our analysis reveals that French companies are structurally disadvantaged in this new economy of algorithmic recommendation. The quantitative study we present here, conducted on 857 commercial queries distributed among twenty French leaders of the CAC40 and Next40, establishes for the first time the precise measure of this asymmetry. The results are final: on average, French champions are absent in 27.2% of the responses produced by the three language models tested during the study (OpenAI GPT-5-mini, Perplexity AI Sonar Pro, Mistral Large Latest). Even more worrying, this invisibility is neither uniform nor random: it hits B2B technology companies with particular violence, the very ones that carry the ambition of an exporting and sovereign French Tech.

This study aims to provide a first quantification of the magnitude of the phenomenon, to identify its mechanisms, and to propose a path to resolution through optimization for generative engines — an emerging discipline that we designate under the acronyms GEO (Generative Engine Optimization) or AEO (Answer Engine Optimization). Beyond the diagnosis, our ambition is to provide economic and political decision-makers with the factual elements necessary for a strategic realization: in the battle for visibility in the AI economy, the French lag is neither a technological fatality nor a cultural determinism, but the fruit of a semantic infrastructure deficit that there is still time to fill.

1. One in Four French Champions Disappears from Artificial Intelligence Responses

1.1. The Key Figure: Invisibilized in More Than a Quarter of Queries

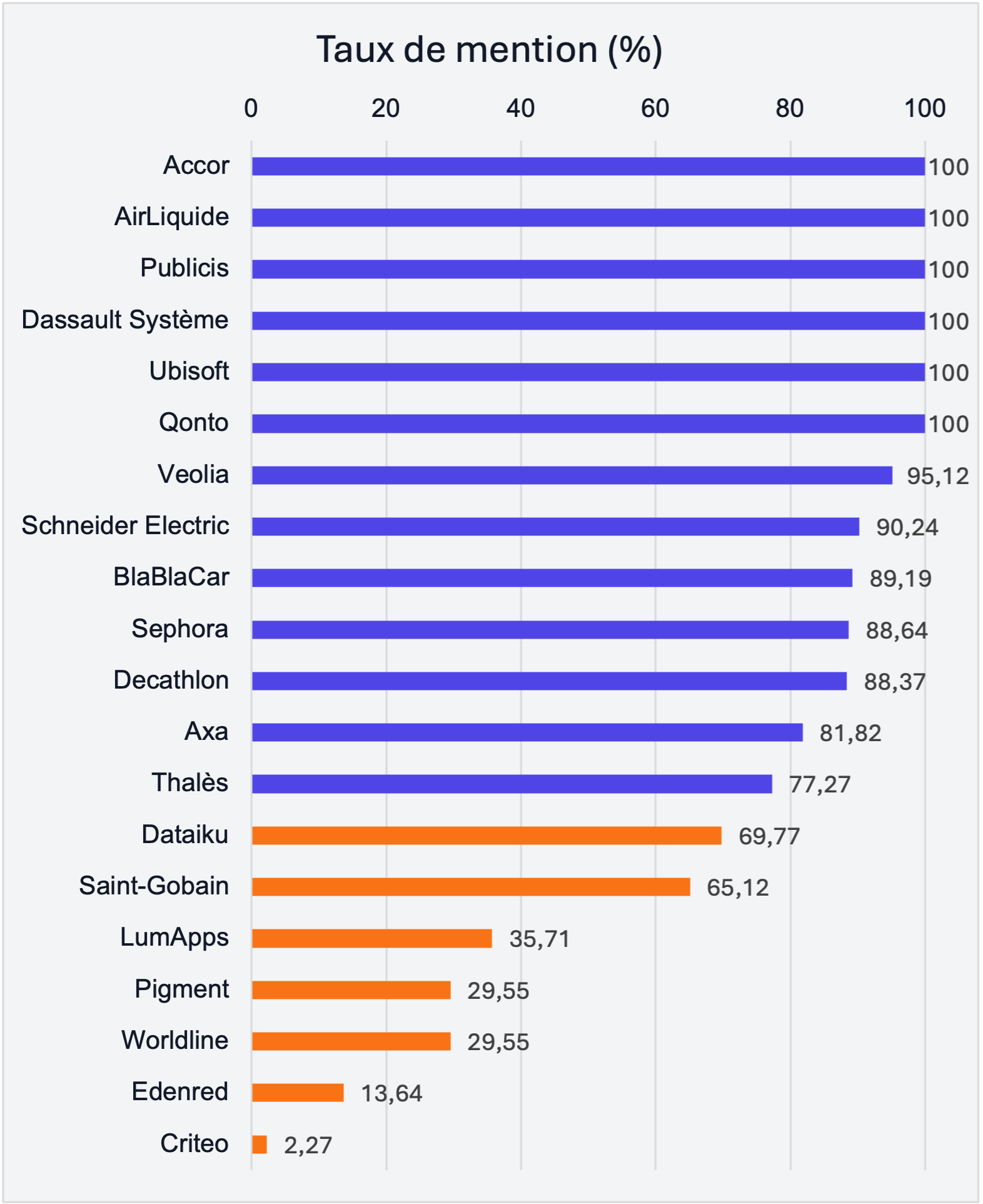

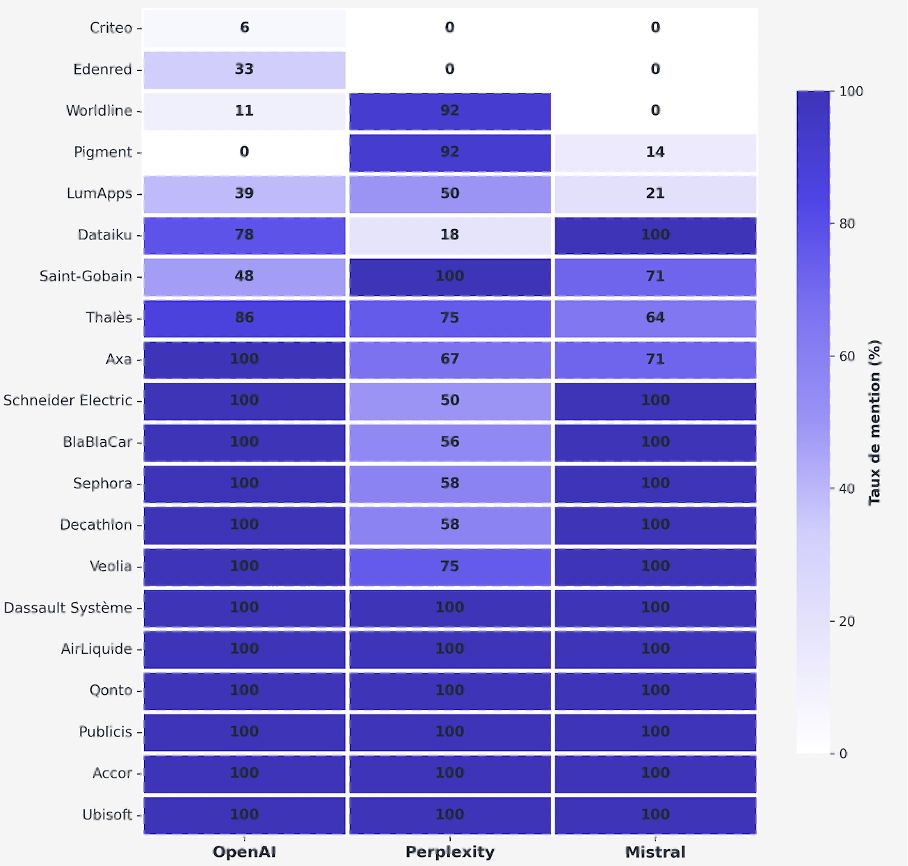

The Artificial Invisibility Index (AII) that we have developed measures the frequency with which a given company is not cited by language models in responses to commercial queries relevant to its sector. Across our entire corpus of 857 queries equitable distributed among twenty leading companies (see Annex 1), the average mention rate stands at 72.81%, which corresponds to a global AII of 27.19%. In other words, out of one hundred queries formulated by potential prospects looking for solutions in their field of activity, French champions do not even appear in the response in more than a quarter of cases.

This aggregated figure, however, masks significant disparities. At the upper end of the spectrum, six companies reach a mention rate of 100%: Accor, Air Liquide, Publicis, Dassault Systèmes, Ubisoft, and Qonto are systematically cited when queries concern their respective sectors. These exemplary performances demonstrate that optimal visibility in AI responses is perfectly achievable for French actors. But at the other end, the situation borders on digital erasure: Criteo, world leader in programmatic advertising on the open web, appears in only 2.27% of responses related to its market. Edenred, world leader in meal vouchers and prepaid payment solutions, caps at 13.64% mention rate. Worldline and Pigment, respective champions of European payment services and enterprise financial planning, stagnate at 29.55% visibility.

The magnitude of these gaps invalidates the hypothesis of a systemic anti-French bias. If that were the case, the distribution of performances would be homogeneous. However, it is not: broadly, it reveals an intra-French fracture whose dividing lines deserve a more detailed analysis. The first pertinent divide is neither geographical nor capitalistic, it is sectoral, as the following section demonstrates.

1.2. The Sectoral Fracture: The Erasure of Technological B2B

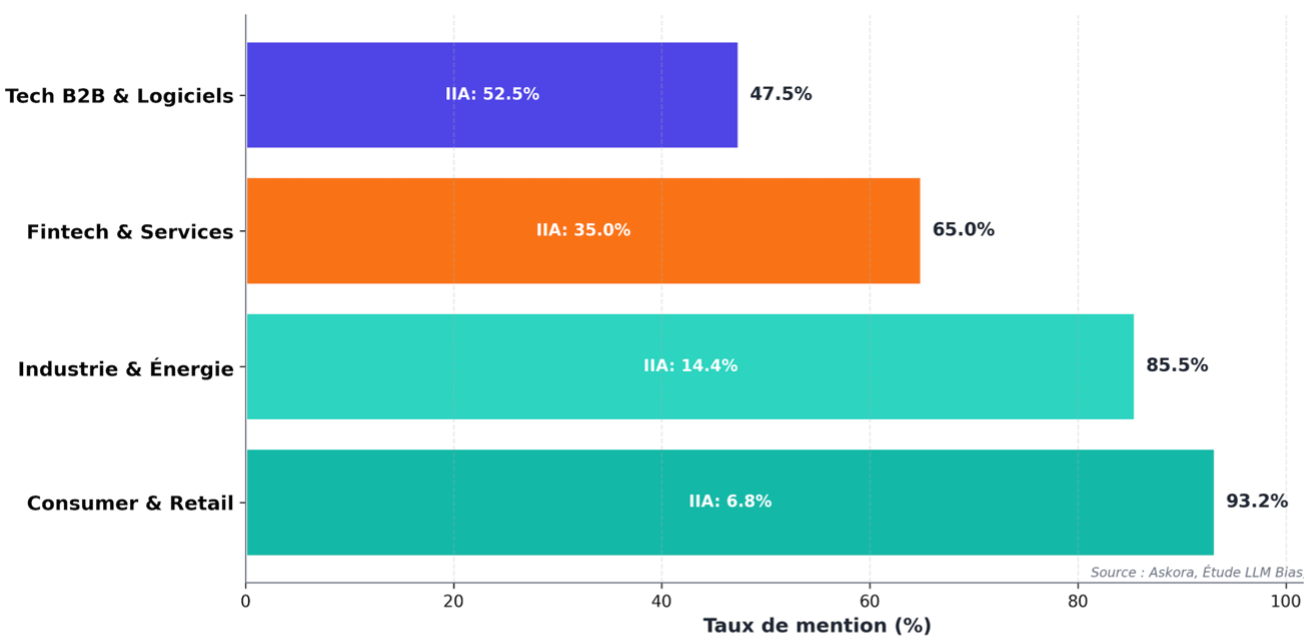

The analysis of performance by sector reveals a robust correlation between the nature of the activity and the degree of visibility in generative responses. The Consumer & Retail sector, which includes Decathlon, Sephora, Ubisoft, Accor, and BlaBlaCar, displays an average mention rate of 93.24%: a residual AII of only 6.76%. These companies, whose products or services address the general public directly, benefit from sustained media presence, abundant commercial documentation, and a diversified digital footprint that facilitates their indexing by language models. Their visibility in AI faithfully reflects their notoriety in the public space.

The Industry & Energy sector (Schneider Electric, Air Liquide, Veolia, Saint-Gobain, Thales) maintains honorable performances with 85.55% mention rate and 14.45% AII. These large industrial groups, often century-old, possess extensive technical documentation, exhaustive financial reports, and an institutional presence that ensures their referencing in model training corpora.

The stall begins with the Fintech & Services sector (Qonto, Worldline, Edenred, Publicis, AXA), whose average mention rate drops to 65%, i.e., 35% invisibility. But it is in the Tech B2B & Software segment that the situation becomes critical: with a mention rate of only 47.46%, this sector records an AII of 52.54%. In other words, more than one in two responses purely and simply ignores the existence of Dassault Systèmes, Criteo, Dataiku, Pigment, or LumApps.

This hierarchy exactly reverses that of the stated political ambitions. While the French Tech strategy relies precisely on these B2B technological champions to conquer international markets, it is they who suffer from the lowest algorithmic recognition. The structural explanation for this paradox lies in the very nature of their activity: complex software solutions intended for specialized professional audiences mechanically generate less general public content, less generalist media coverage, and fewer discussions on open forums than everyday consumer products. Yet it is precisely these sources (press, social networks, forums, etc.) that constitute the raw material of LLM training corpora. B2B tech companies thus find themselves trapped in a vicious circle: their weak footprint in the open internet makes them invisible to models, which reduces their capacity to reach new customers via emerging conversational channels just as much, and ultimately reducing the probability of obtaining reviews or mentions by users in future training data.

1.3. The Artificial Downgrade Index: Being Cited Does Not Mean Being Recommended

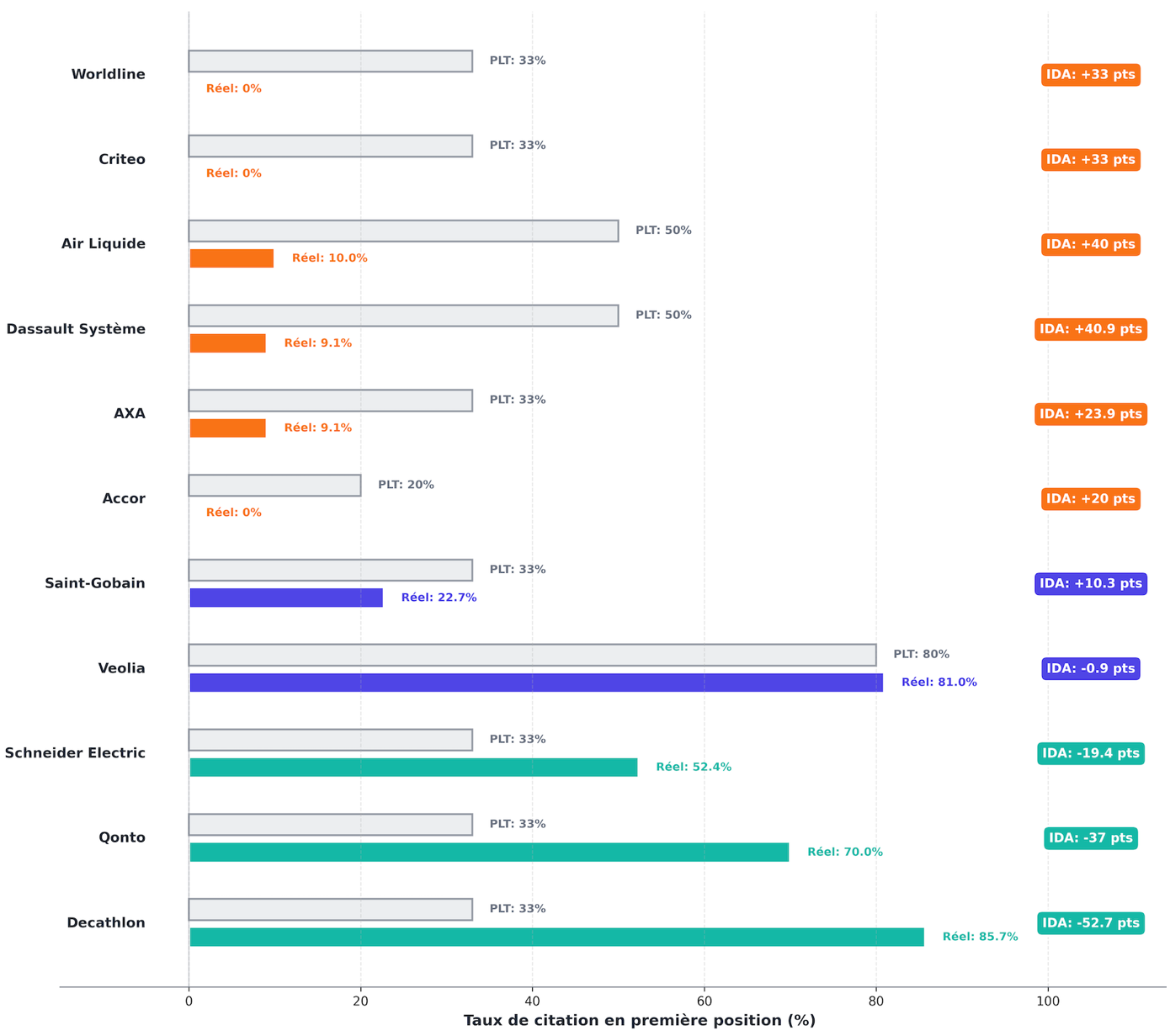

Beyond simple presence in AI responses, the citation position constitutes a major determinant of effective lead capture. When a language model generates a comparative response citing three to five actors, the company mentioned in the first position mechanically captures disproportionate attention: by cognitive anchoring effect in the reader, but also by algorithmic presentation bias on certain interfaces that highlight the first result. To measure this effect, we developed the Artificial Downgrade Index (ADI), which quantifies the gap between the leadership position a company should theoretically occupy given its actual market share, and its effective position in algorithmic citations (see Annex 2).

The calculation of the ADI relies on the notion of Theoretical Leadership Share (TLS). For each company, we established a citation benchmark in the first position expected according to the competitive structure of its market: 80% for a quasi-monopolistic leader (Veolia post-merger with Suez), 50% for a dominant co-leader (Air Liquide, Dassault Systèmes), 33% for a leading actor in an oligopoly of three (AXA, Decathlon, Dataiku), 20% for a leader in a very competitive market (Accor, Worldline). The ADI is then calculated as the difference between this TLS and the observed citation rate in the first position: a positive ADI signals a downgrade (the company is less often cited first than it should be), a negative ADI reveals largely algorithmic outperformance.

The global results show a moderate but significant structural downgrade: on the entire corpus, the average ADI stands at nearly 16 points. In other words, French companies are cited in first position approximately 16 percentage points less often than their actual market position would justify. This ranking penalty is added to the pure invisibility measured by the AII: not only do some companies not appear in a quarter of responses, but when they do appear, they are frequently relegated to a secondary position.

The analysis of the ADI reveals three categories of companies with radically distinct profiles. The first brings together algorithmic outperformers, who benefit from a significant negative ADI — that is, they are cited in first position substantially more often than their theoretical market share would justify. Decathlon dominates this category with an ADI of -46 points: while its TLS in competitive sports retail is only 33%, the Northern brand reaches nearly 80% of citations in first position. Sephora with -23 points, Qonto with -22 points, Schneider Electric with -18 points. These companies have managed to build algorithmic authority that exceeds their real market weight, becoming the spontaneous references of language models in their respective sectors. Their success reveals that an extensive content strategy can compensate for a less dominant competitive positioning and transform a company into the "default choice" of algorithms.

Conversely, the second category brings together the critical downgrades, whose ADI reaches the theoretical ceiling (for example when the TLS is 33% and the citation rate in first position is 0%) or approaches it strongly. This situation concerns nine out of twenty companies: Criteo, Edenred, Worldline, LumApps, BlaBlaCar, Accor, Axa, Thales, Dassault Systèmes, and Air Liquide. Criteo illustrates this phenomenon dramatically: although a world leader in programmatic advertising, the company is never recommended as a priority by LLMs, which systematically prefer other actors (often American like The Trade Desk) even though they are less dominant technically. This systematic relegation transforms Criteo's residual presence (2.27% mention rate) into commercial quasi-invisibility: a prospect reading a response mentioning Criteo in third or fourth position after two American competitors would likely retain the latter.

The third category, that of moderate downgrades, brings together companies whose ADI is significant but who nevertheless manage to be cited in first position significantly: Saint-Gobain (33 points), Publicis (33 points), Dataiku (21 points), Ubisoft (10 points). These actors maintain an honorable presence in terms of global mention rate, but their citation position does not reflect their sectoral leadership. Saint-Gobain, world leader in construction materials, should theoretically be cited first in 33% of queries related to its market: it is only cited in 22.73% of cases in French and 9.52% in English, revealing that models perceive it as one actor among others rather than as the undisputed leader that it objectively is.

The major lesson of the ADI analysis can be summed up in one formula: in the AI economy, being present is no longer enough, you must be recommended as a priority. However, this algorithmic priority does not flow mechanically from actual market share. It results from the narrative authority that the company has managed to build in the model source corpora. Outperformers like Decathlon, Veolia, or Qonto share a common point: an extensive content strategy, abundant public documentation, a sustained media presence that have saturated the open internet with authority signals. Conversely, critical downgrades like Criteo or Worldline have probably neglected this dimension, favoring closed commercial communication to the detriment of building a public semantic footprint. Algorithmic downgrade is therefore not a technical fatality but the symptom of a strategic deficit of investment in narrative visibility.

1.4. The Bias of Linguistic Ghettoization: A Brake on Internationalization

Beyond the sectoral fracture, our study reveals the existence of a phenomenon that we qualify as "linguistic ghettoization": algorithmic discrimination based on the language in which the query is formulated. For each company in our sample, we submitted strictly equivalent prompts in French and English to the three models tested. Comparative analysis reveals a systematic bias, certainly moderate in absolute value but strategically decisive.

On the entire corpus, the average mention rate in French stands at 73.20%, against 72.47% in English. This is a difference of 0.73 points at first glance negligible, but which in reality is significant. When we measure not simple mention but citation position in rank number one in the generated responses, the gap widens significantly: 23.49% of citations in first position for queries in French, against only 19.00% for queries in English. The Artificial Downgrade Index (ADI) that we designed allows analyzing the downgrade suffered by French brands relative to their theoretical leadership. Thus, while French companies suffer an ADI downgrade of 13 points on queries in French, this increases to 18 points in English, i.e., an increase of more than 35% in the artificial downgrade index when switching from French to English.

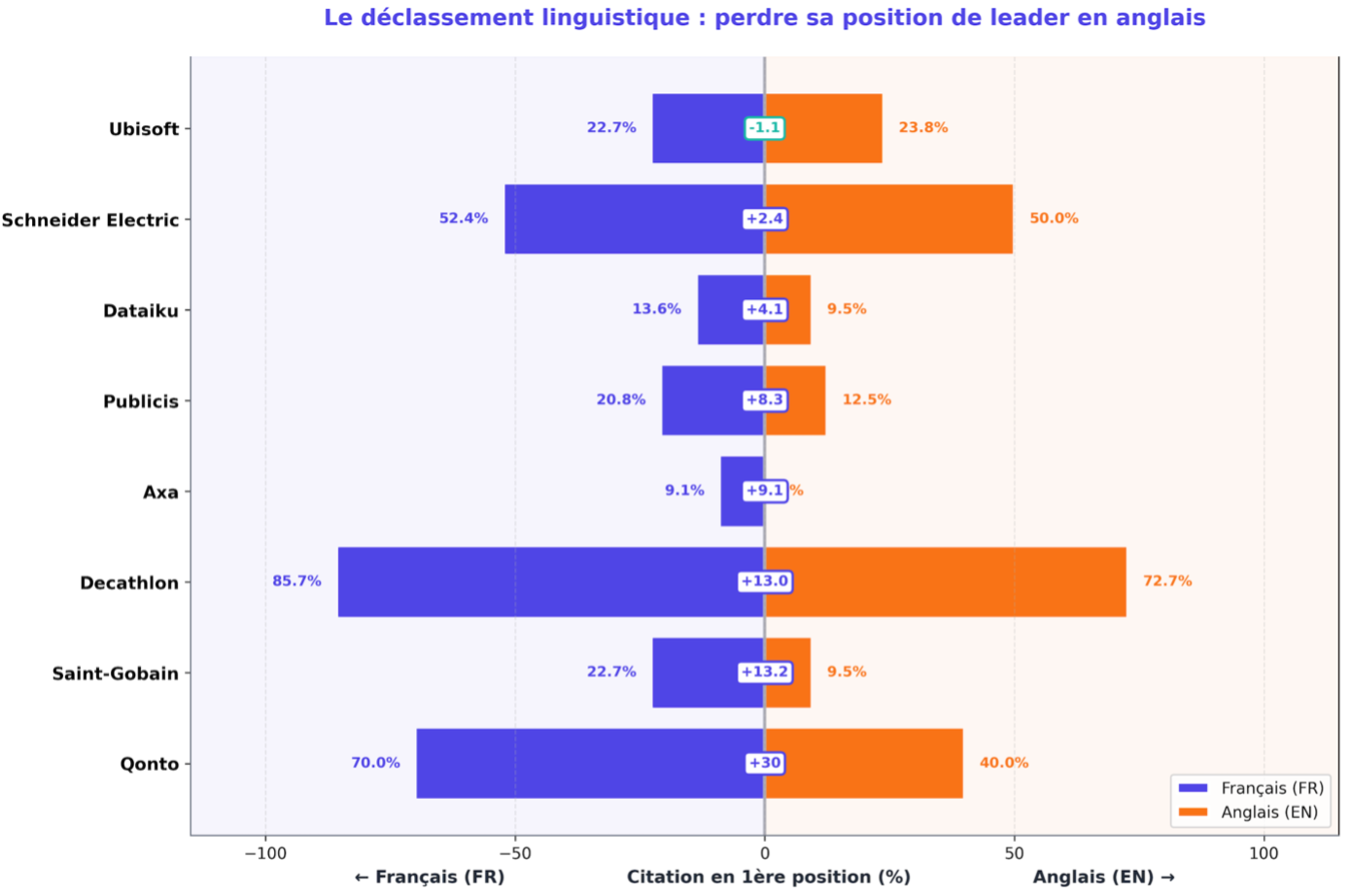

This linguistic visibility penalty does not affect all companies uniformly. Some of them experience real situations of "domestic ghetto": Edenred displays 27.3% mention rate in French queries, but falls to 0% in English queries. AXA goes from 95.5% in French to 68.2% in English, a drop of 27 points. Decathlon retreats 22.7 points between the two languages. Conversely, some companies paradoxically benefit from an "Anglophone visibility bonus": Thales progresses by 29.4 points in English compared to French (61.9% vs. 91.3%), Sephora gains 22.7 points, Schneider Electric 19 points.

In terms of downgrade, linguistic bias is also unequal. Actors like Veolia, Sephora, or Dassault Systèmes show remarkable immunity to linguistic bias in terms of downgrade: Veolia maintains a quasi-identical leadership position with 80.95% of citations in first position in French against 80% in English (gap of 0.95 points), Sephora displays perfect stability at 72.73% in both languages, and Dassault Systèmes keeps exactly the same rate of 9.09% regardless of the query language on the tested prompts. These companies, often historical multinationals having invested massively in bilingual technical documentation of equivalent quality, demonstrate that a truly international content strategy neutralizes the linguistic penalty.

On the other hand, other actors suffer a severe downgrade in leader position despite a correct mention: Qonto, although maintaining a mention rate of 100% in both languages, sees its citation rate in first position collapse from 70% in French to 40% in English, thus losing 30 points of leadership. Decathlon, although cited systematically, retreats from 85.71% to 72.73% in position #1 between French and English. Saint-Gobain goes from 22.73% to 9.52%, i.e., a division by 2.4 of its algorithmic leadership. These companies illustrate an insidious phenomenon: being present is not enough, one must still be recommended as a priority, and this priority erodes massively when the query is formulated in English, which hinders the construction of international leadership.

Interpreting these data requires going beyond simplistic explanations. It is not an anti-French bias programmed into the algorithms; the presence of the "Anglophone bonus" for certain companies or a "linguistic neutrality" for others invalidates this hypothesis. The mechanism at work is more subtle: language models reflect the distribution of content available in their training corpora and online. Yet these corpora, dominated by the Anglophone internet (estimated at 60% of total web content versus less than 5% for French according to W3Techs), mechanically overrepresent Anglophone sources. French companies whose authority documentation (detailed case studies, technical white papers, expert opinion pieces in reference media, etc.) exists only in French, or whose English versions are poor, poorly referenced, or confined to paid spaces, effectively find themselves penalized in leadership position when an international user formulates their query in English.

The particular case of Qonto perfectly illustrates this issue: with an identical mention rate of 100% in French and English, this neobank demonstrates that a truly bilingual content strategy neutralizes the linguistic handicap. But its citation rate in first position drops from 70% in French to 40% in English, revealing that even identical quantitative visibility does not guarantee equivalent qualitative positioning. For French companies aspiring to international growth, this linguistic ghettoization constitutes a direct brake: while 46% of B2B decision-makers declare using ChatGPT or an equivalent for their solution research (The Insight Collective, B2B Tech Buyer Behavior, 2025), being invisible in English responses amounts to voluntarily excluding oneself from international markets.

1.5. The Algorithmic Lottery: The Illusion of Objectivity

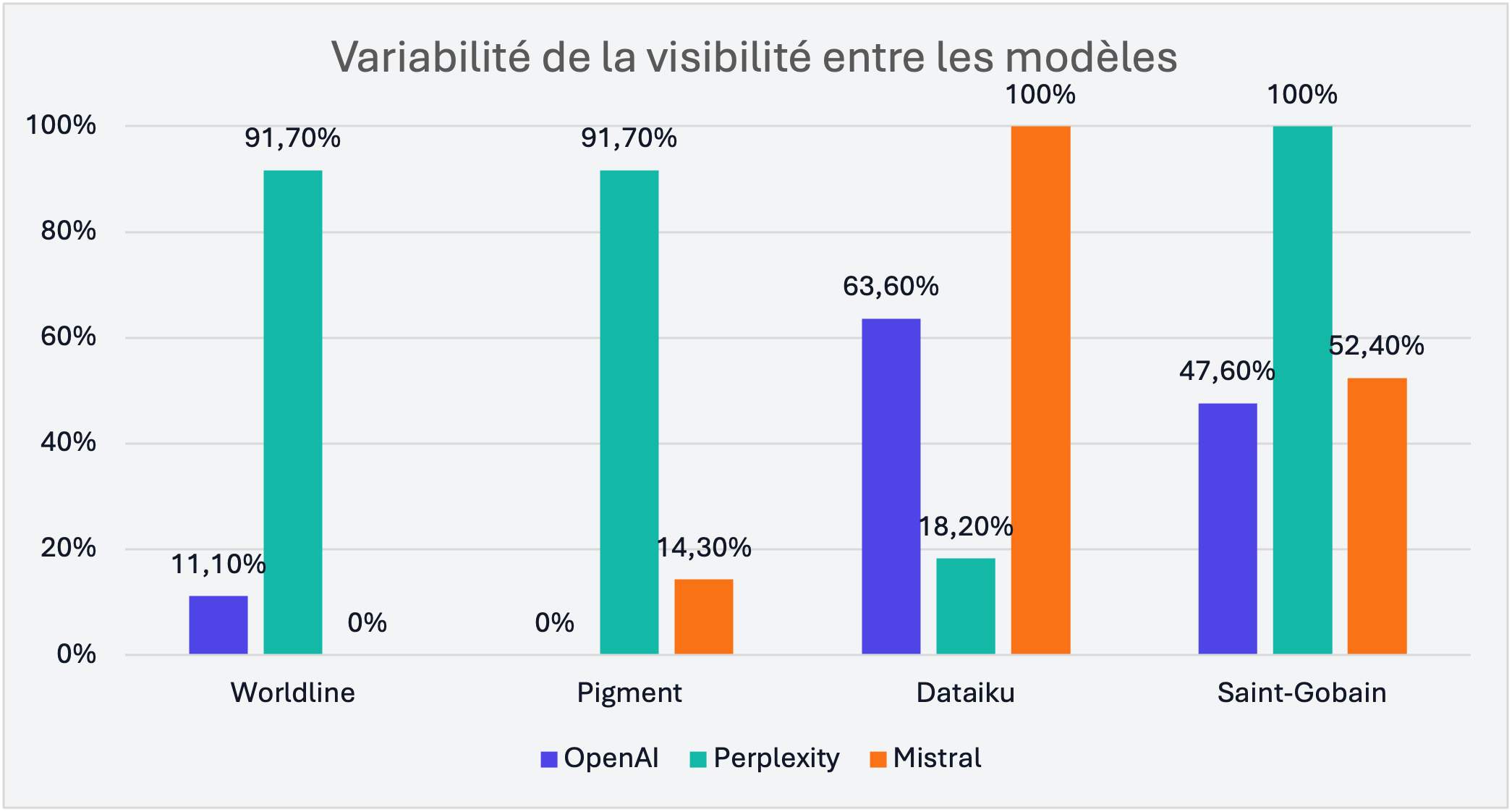

A final lesson from our study invalidates the idea that language models would produce objective and convergent recommendations. The analysis of performance variations of the same company according to the model queried reveals, on the contrary, a form of "algorithmic lottery": visibility gaps reaching up to 91.7 percentage points depending on whether the query is addressed to OpenAI, Perplexity, or Mistral.

Worldline constitutes the paradigmatic example: this company displays a mention rate of 91.7% when Perplexity AI answers the query, but falls to 0% when the same query is submitted to Mistral. Pigment experiences identical volatility, going from 91.7% on Perplexity to 0% on OpenAI. Dataiku oscillates between 100% visibility on Mistral and 18.2% on Perplexity. These extreme variations cannot be explained by differences in legitimacy or relevance (the companies concerned are objectively leaders in the segment tested) but rather by the heterogeneity of the source corpora and retrieval mechanisms of each model.

This fragmentation creates unprecedented strategic uncertainty: where a company could previously optimize its presence for a dominant search engine (Google capturing 92% of the European market), it must now manage a multiplicity of conversational channels whose indexing logics diverge radically. The risk is twofold: on the one hand, the impossibility of predicting which model will be used by a given prospect makes any partial optimization strategy potentially counterproductive; on the other hand, the rapid crystallization of user preferences risks creating lock-in effects, where companies absent from the responses of a model in the ramp-up phase find themselves permanently excluded from its user base.

The three models tested also present distinct citation profiles: OpenAI displays the highest global mention rate (75.03%) and frequently cites companies in first position (26.53%), suggesting a broad corpus and multiple citation logic. Perplexity, although less generous in global mention rate (69.52%), distinguishes itself by an extreme diversification strategy: its citation rate in first position falls to 2.50%, revealing a tendency to systematically propose multiple alternatives rather than a single leader. Mistral, finally, occupies an intermediate position (72.14% global mention) but proves to be the most generous in first-rank citations (27.86%), perhaps out of a desire to decide more clearly between options.

These divergent profiles prohibit any single-channel strategy. Optimization for one of the models guarantees visibility on the others in no way. This algorithmic fragmentation, if not rapidly mastered by French companies, risks further accentuating their lag: while they discover the existence of the problem, their American competitors - whose massive presence in Anglophone corpora ensures basic visibility on all models - are already accumulating a comparative advantage difficult to catch up with.

2. From Invisibility to Revenue Loss: How AI Will Cost €6 Billion to French Champions

2.1. From Invisibility to Revenue Loss: A Necessary Extrapolation

Quantifying the economic impact of algorithmic invisibility requires projecting the migration of commercial traffic from traditional search engines to conversational AI interfaces. Traffic data consolidated over the last quarter of 2025 indicate that about 10% of searches are now carried out via LLMs rather than via Google. This proportion, still marginal, is experiencing exponential growth: according to aggregated average projections from Gartner, it will reach 30% in 2026, and would cross the 50% mark before 2028.

To model the impact of this transition, we built a three-step methodology. First, we estimated the share of each company's turnover generated via digital acquisition: a proportion varying by sector between 30% (heavy industry) and 60% (pure players B2B tech). Second, we applied the migration rate to LLMs to this digital share: in 2026, with 30% migration, this means that 30% × digital_share of turnover now transits through conversational channels. Third, we multiplied this flow by each company's AII: if Criteo is invisible in 97.73% of responses, it mechanically loses 97.73% of prospects using this channel.

On this basis, and retaining the median scenario (30% migration in 2026, average sectoral digital share), the collective revenue loss of the twenty analyzed companies would amount to €5.99 billion in 2026. AXA, given its massive turnover (€102 billion) and its moderate but non-negligible AII (18.2%), alone concentrates €1.95 billion of potential loss. Saint-Gobain, despite an AII contained at 34.9%, sees its shortfall reach €1.50 billion due to its turnover of €47.9 billion. Worldline, with a catastrophic AII of 70.5% but a more modest turnover of €4.6 billion, loses €583 million. Criteo, the most critical case, records a shortfall of €334 million: i.e., 17.6% of its total turnover.

This extrapolation relies on a strong hypothesis: proportionality between algorithmic invisibility and loss of prospects. This hypothesis is debatable, a particularly motivated prospect may compensate for the lack of AI recommendation by active research, but it remains conservative nonetheless. On the one hand, it does not take into account the downgrade effect (ADI): a company cited in fourth position in a ChatGPT response likely captures fewer leads than if it appeared first, but our model treats these two situations as equivalent. On the other hand, it ignores the preference crystallization effect: the more a model systematically recommends actor A rather than actor B, the more the relative notoriety of A increases, which reinforces its probability of being recommended in subsequent iterations, creating a "snowball effect" dynamic that our linear model does not capture.

If we extend the exercise to the 2028 horizon with a migration rate raised to 50%, the collective shortfall reaches €9.99 billion. Over the cumulative period 2024-2026, taking into account the gradual progression of the phenomenon, the total impact approaches €18.9 billion. These orders of magnitude, even with a substantial margin of uncertainty, suffice to qualify algorithmic invisibility not as a marketing inconvenience but as a top-tier strategic risk.

2.2. The Defensive Marketing Cost: Compensating Organic with Paid

Beyond the direct shortfall in terms of lost leads, invisibility in AI responses generates a second economic effect: the obligation to invest more in paid advertising (search engine advertising, display, social ads) to compensate for the loss of organic visibility. In the traditional search economy, a company well-referenced naturally could limit its SEA expenses to the most competitive keywords. In the conversational economy, a company systematically absent from generative responses will have to buy almost all of its traffic.

This additional cost presents a particular characteristic: the marketing surcharge constitutes a rent paid to advertising platforms (Google Ads, Meta, LinkedIn, tomorrow LLM companies if they offer this service) which can only be avoided by solving the problem at the root, that is to say by optimizing presence in LLM source corpora. In other words, algorithmic invisibility creates a structural dependency on paid channels, permanently transferring value from producing companies to advertising intermediaries.

2.3. competitive Asymmetry France - United States: The Rent of Linguistic Hegemony

The economic analysis would be incomplete without integrating the geostrategic dimension of French invisibility. Although our study did not include a control group composed of American companies (a methodological limit we recognize), several convergent indicators suggest the existence of a structural asymmetry unfavorable to French actors.

First, the overrepresentation of English in LLM training corpora (60% vs. <5% for French) mechanically confers a basic visibility advantage to companies natively producing content in English. Second, dominant models (OpenAI, Anthropic, Gemini) are developed by American companies whose training teams, testers, and early adopters evolve predominantly in the Anglo-Saxon ecosystem, creating sampling biases even if unintentional. Third, privileged data partnerships formed by these actors (Reddit for OpenAI, Stack Overflow for diverse models, American media) further reinforce the overrepresentation of US content.

This asymmetry transforms linguistic hegemony into economic rent. While Criteo, world leader in programmatic advertising, must invest massively to attempt to appear in ChatGPT responses, its American competitors, less dominant technically, benefit from superior algorithmic visibility simply due to their linguistic and editorial environment. The "visibility discount" suffered by French companies is therefore not only a technical optimization problem, it is a competitive disadvantage that progressively erodes their market shares internationally, precisely at the moment when national strategy is banking on their expansion outside France.

The risk, ultimately, is that of a structural stall: if positions in AI responses crystallize quickly ("snowball effect" mentioned previously), and if French companies lag several years behind in awareness and implementation of AEO / GEO strategies, they could find themselves permanently confined to their domestic or regional markets, while their American and Chinese competitors capture the bulk of global growth via their superior algorithmic visibility. Invisibility in AI would then no longer be a simple marketing problem, but a structuring factor of 21st-century geo-economics.

3. Why Do LLMs Not Cite French Companies?

3.1. The Gap in Semantic Infrastructures: Knowledge Graphs versus PDF Documentation

The first structural cause of French invisibility lies in the semantic infrastructure gap separating the American and French digital ecosystems. Since the mid-2010s, large American technology companies have massively invested in building Knowledge Graphs: structured databases describing entities, their attributes, and their relationships in a form directly exploitable by algorithms. Google Knowledge Graph, launched in 2012, now lists more than 500 billion structured facts, and Microsoft, Amazon, Facebook have developed their own sectoral semantic graphs. These infrastructures serve as skeletons for language models: when an LLM answers a factual question, it does not content itself with identifying statistically probable word sequences, it often performs a retrieval in these graphs or structured data to anchor its response in verified facts.

Conversely, French companies, including CAC40 champions, have historically favored a logic of closed documentation. Their strategic information is recorded in PDF annual reports (difficult to index), institutional sites in Flash or JavaScript difficult to read by indexing robots, press releases hosted on proprietary platforms, or even intranets entirely closed to the public. This culture of confidentiality, inherited from an era when information was a strategic asset to protect, turns against these companies today: what is not structured and publicly accessible simply does not exist for language models. It is not about European champions building their own Knowledge Graphs but adopting a logic of open documentation in order to be better represented in the Knowledge Graphs of American giants.

The case of Criteo perfectly illustrates this paradox. This company has exhaustive technical documentation, but mostly confined to authenticated client portals, private webinars, and whitepapers downloadable only after filling out a commercial form. Conversely, its American competitors like The Trade Desk, more transparent in their communication, saturate the open internet with use cases, expert opinions, and educational content freely accessible. Thus, Criteo remains invisible to the eyes of crawlers that feed training corpora.

3.2. The Culture of Documentation: American Transparency vs. French Discretion

Beyond infrastructure, it is a deep cultural difference that explains the visibility gap. Anglo-Saxon corporate culture, driven mainly by the United States and the United Kingdom, values documentary transparency as a tool for legitimation and recruitment: exhaustively publishing one's methodology, sharing performance metrics (including failures), publicly documenting technical architecture is not a risk but a brand strategy. Silicon Valley tech companies have taken this logic to its paroxysm with the "default to open" doctrine: unless justified exception, all information is public by default.

This culture has produced an Anglophone internet extremely dense in quality technical documentation: Stack Overflow counts 23 million questions-answers in English against 400,000 in French; GitHub hosts 85% of its repositories in English; specialized forums, tutorial YouTube channels, expert podcasts are massively Anglophone. This asymmetry far exceeds the simple demographic effect: if we adjust for the size of B2B tech populations (about 1.5 billion Anglophone professionals against 100 million Francophones, i.e., a ratio of 15×), the ratio observed on Stack Overflow (57.5×) reveals an overrepresentation of Anglophone content by a factor of 3.8, indicating not only a volume advantage, but a qualitative difference in documentary practices. Companies evolving in the Anglophone ecosystem thus produce, for an equal population, substantially more publicly accessible technical content than their Francophone counterparts.

This density creates a virtuous circle for Anglophone companies (and particularly American ones): the more they document, the more visible they are in searches, the more they attract talent and clients, the more they document. Conversely, French corporate culture values discretion, control of information, and a certain form of strategic mystery. Publishing in detail internal processes, operational difficulties, or technological trade-offs is perceived as a vulnerability rather than an asset. This cultural difference is neither good nor bad in itself, it reflects distinct managerial traditions, but it becomes penalizing in a world where algorithmic visibility relies precisely on the density of accessible public content.

This logic is confirmed by the most visible French companies in our study (Decathlon, Veolia, Air Liquide), which are precisely those that have, for years, adopted content strategies close to Anglo-Saxon standards: active corporate blogs, institutional YouTube channels, presence on LinkedIn, technical documentation in open access. Conversely, the most invisible (Criteo, Worldline) have rather had closed communication strategies, oriented towards direct commercial relations rather than broad diffusion: strategies that worked in the traditional search economy but condemn them to invisibility in the generative model economy.

3.3. Investment Lag: SEO Acquired, GEO Non-Existent

The third cause of the French lag lies in the time gap between the emergence of a problem and its strategic management. In the field of Search Engine Optimization (SEO), French companies initially lagged three to five years behind their American counterparts in the 2000s, before catching up during the 2010s. Today, most French champions have mature SEO teams, specialized consultants, and budgets dedicated to Google optimization.

But Generative Engine Optimization (GEO) or Answer Engine Optimization (AEO), a sister discipline aimed at optimizing presence in LLM responses, is still at an embryonic stage in France. While specialized actors are emerging in the United States since 2023 and some American companies have already internalised "Heads of AI Visibility", the French ecosystem remains largely unaware of the problem.

This investment lag is not irremediable, it simply reflects the recent nature of the disruption, but it is growing increasingly. Every month that passes without optimization reinforces the positions of competitors already visible ("snowball effect"), makes algorithmic ascent more costly (saturation of source corpora), and increases the skills gap between already trained American teams and French teams still to be trained. The risk is that by the time awareness occurs, the lag will have become structurally insurmountable, as was the case for some European companies that, having neglected SEO until 2015, were never able to catch up on strategic queries saturated by American competitors for fifteen years.

3.4. A Fatality? No, A Reversible Infrastructure Problem

It would be tempting to conclude that French invisibility in the AI economy constitutes a technological or cultural fatality. This conclusion would be erroneous. Our study demonstrates on the contrary that French companies can achieve optimal visibility: six of them display a mention rate of 100%, proving that no systemic glass ceiling limits French actors. The difference between Accor (100% visibility) and Worldline (29.55%) lies neither in their nationality, nor their size, nor their sectoral legitimacy: it lies in their digital content strategy.

Similarly, the "Anglophone bonus" enjoyed by certain French companies (Thales, Schneider Electric, Sephora) when queried in English invalidates the hypothesis of a programmed anti-French bias. These companies have not become Anglo-Saxon, they have simply invested in the production of Anglophone content or adapted to English indexing of quality, correctly structured and widely disseminated.

French invisibility is therefore neither a linguistic fatality, nor a cultural determinism, nor an insurmountable technical handicap. It is a reversible digital infrastructure problem, provided one acknowledges its existence, understands its mechanisms, and allocates appropriate resources. The following section presents the paths to resolution.

4. Generative Engine Optimization (GEO): Translating French Excellence into Algorithmic Visibility

4.1. Definition and Scope of Generative Engine Optimization

Generative Engine Optimization (GEO), sometimes also called Answer Engine Optimization (AEO), refers to the set of techniques aimed at optimizing the presence of an entity (company, product, personality) in responses generated by Large Language Models (LLMs). Unlike SEO, which targets search engine result pages (SERP), GEO targets synthetic responses produced by conversational models. This difference in target implies a difference in method.

SEO relies on three pillars: technical site optimization (speed, crawlability, indexation), content optimization (keywords, semantic structure, freshness), and authority optimization (backlinks, citations, reputation). GEO retains these three dimensions but transposes them into a new paradigm. Technical optimization becomes semantic structuring: it is no longer about facilitating a robot's crawl, but producing data directly ingestible by models, via structured formats (JSON-LD, Schema.org, proprietary Knowledge Graphs). Content optimization becomes narrative authority: one must no longer place keywords, but build coherent factual narratives, densely sourced, which impose themselves as references in the field. Authority optimization becomes validation by consensus or priority authority: models favor sources cited by multiple independent actors, creating a decentralized reputation system, or sources identified as having a very high authority factor.

Concretely, a GEO strategy for a company like Worldline would imply five simultaneous workstreams. First, the structuring of its key data in standard public accessible semantic formats. Second, the production of high-quality educational content (technical guides, white papers, case studies) disseminated in open access rather than behind forms. Third, the multiplication of expert opinion pieces in third-party media to create very qualitative independent external citations. Fourth, linguistic optimization: systematic English version of equivalent quality to the French version for all strategic content. Fifth, continuous performance monitoring via specialized tools measuring the citation rate in major conversational platforms.

4.2. Strategic Urgency: The Window of Opportunity Is Closing

The decisive argument in favor of immediate mobilization of French companies on GEO lies in the temporary nature of the current window of opportunity. We are today in a transitional phase, which we estimate to last eighteen to thirty-six months, where algorithmic positions are not yet crystallized and easily accessible. Language models continue to be retrained frequently (every three to six months for major versions), their source corpora evolve, and users themselves have not yet stabilized their model preferences. It is in this period of fluidity that it is still possible to modify visibility significantly.

But this window is closing. Several locking mechanisms are at work. The first is the algorithmic reinforcement effect: the more an actor is cited, the more it accumulates new content mentioning this citation (press articles, market studies, forums), which further increases its probability of being cited during the next model training. The second is the corpus saturation effect: as quality public sources become scarce (everything having already been indexed), models accord increasing weight to historically established sources, making it more difficult for new actors to emerge. The third is the user preference crystallization effect: once a B2B decision-maker has internalized that "for payments, ChatGPT always recommends Stripe", they will stop asking the question and go directly to Stripe — even if Worldline has, in the meantime, improved its visibility.

These three mechanisms create a path dependency risk: positions acquired in the next two years could permanently determine the competitive hierarchy of the 2030 decade. Companies that invest in GEO today will benefit from a first-mover advantage difficult to catch up with. Those that delay risk being structurally excluded. The history of SEO offers an instructive precedent: companies that invested massively in Google referencing between 2005 and 2010 continue, fifteen years later, to enjoy dominant positions on strategic queries, simply because they accumulated an unsurpassable capital of authority (backlinks, domain age, content density) for late entrants.

The urgency is therefore not marketing but strategic. It is not about capturing a few extra leads, but preserving the very capacity of the company to be discovered by future generations of clients. In a world where LLM searches will exceed Google searches in volume within 2 to 5 years, algorithmic invisibility progressively equates to invisibility period. French companies that do not correct their visibility deficit by then risk becoming structurally inaccessible to new generations of buyers, condemning, over time, their economic model.

The Role of Nodiris: Translating Excellence into Algorithmic Visibility

It is precisely this strategic need for visibility in AI that Nodiris wishes to solve. As a specialized actor in Generative Engine Optimization, our mission consists of restoring visibility to brands and making AI their new acquisition channel. French companies do not suffer from a deficit of technical skills or innovation, but from a deficit of semantic translation of these skills into the formats and channels favored by language models. A rapid investment by French companies in GEO would allow them to correct their AI visibility deficit.

The window of action is narrow but still open. Companies that do not correct their visibility deficit within 2 to 5 years risk becoming structurally inaccessible to new generations of buyers, condemning over time their capacity to capture new clients on international markets. It is not a question of a few lost leads, but of preserving the very capacity of the company to be discovered by future generations of prospects.

Then, when algorithmic positions have crystallized, compensatory advertising budgets will have become permanent. And the €6 billion shortfall estimated for 2026 will have transformed into €10 billion in 2028. Investing today in one's GEO / AEO is not only a marketing issue but a strategic one.

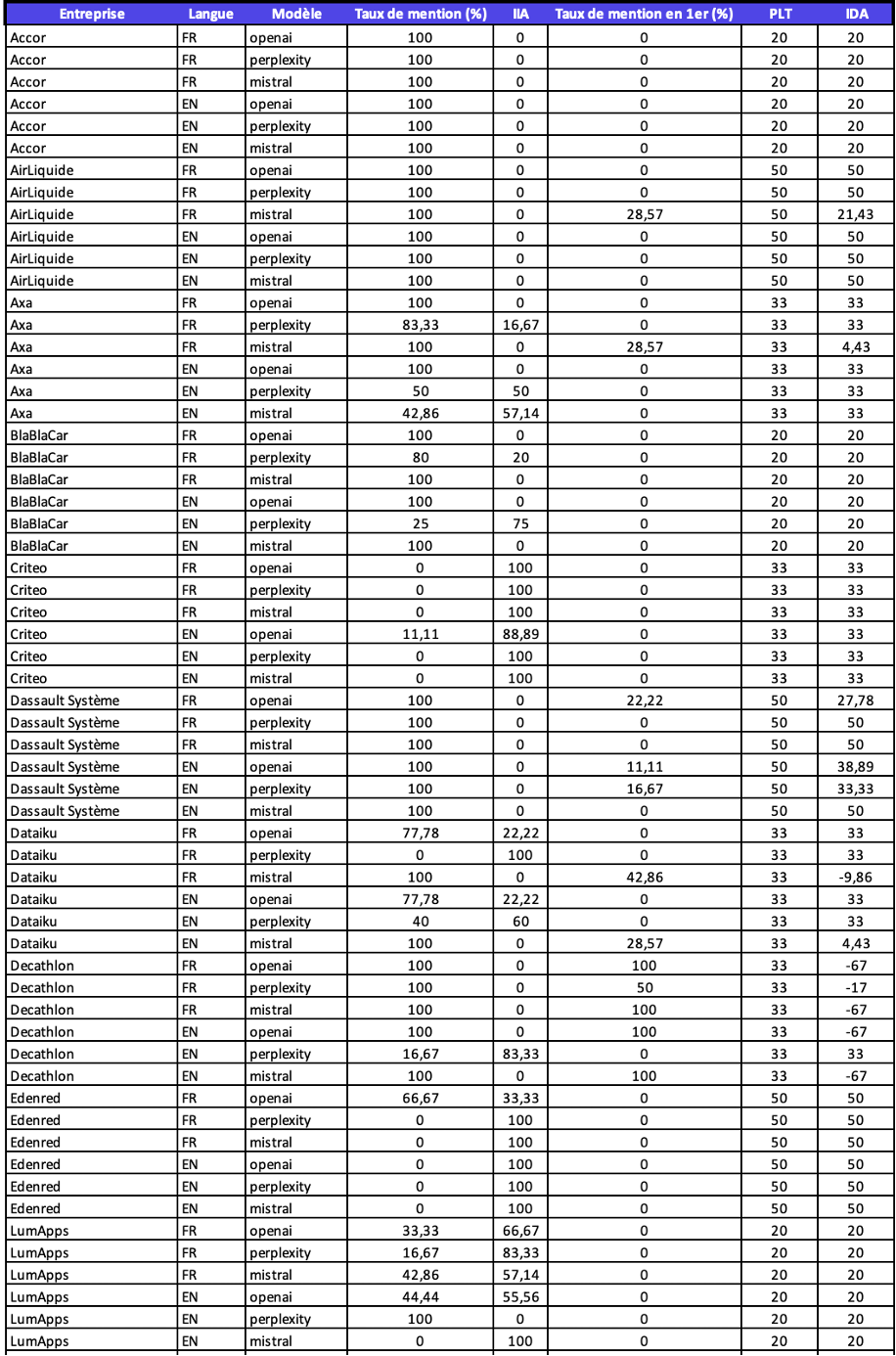

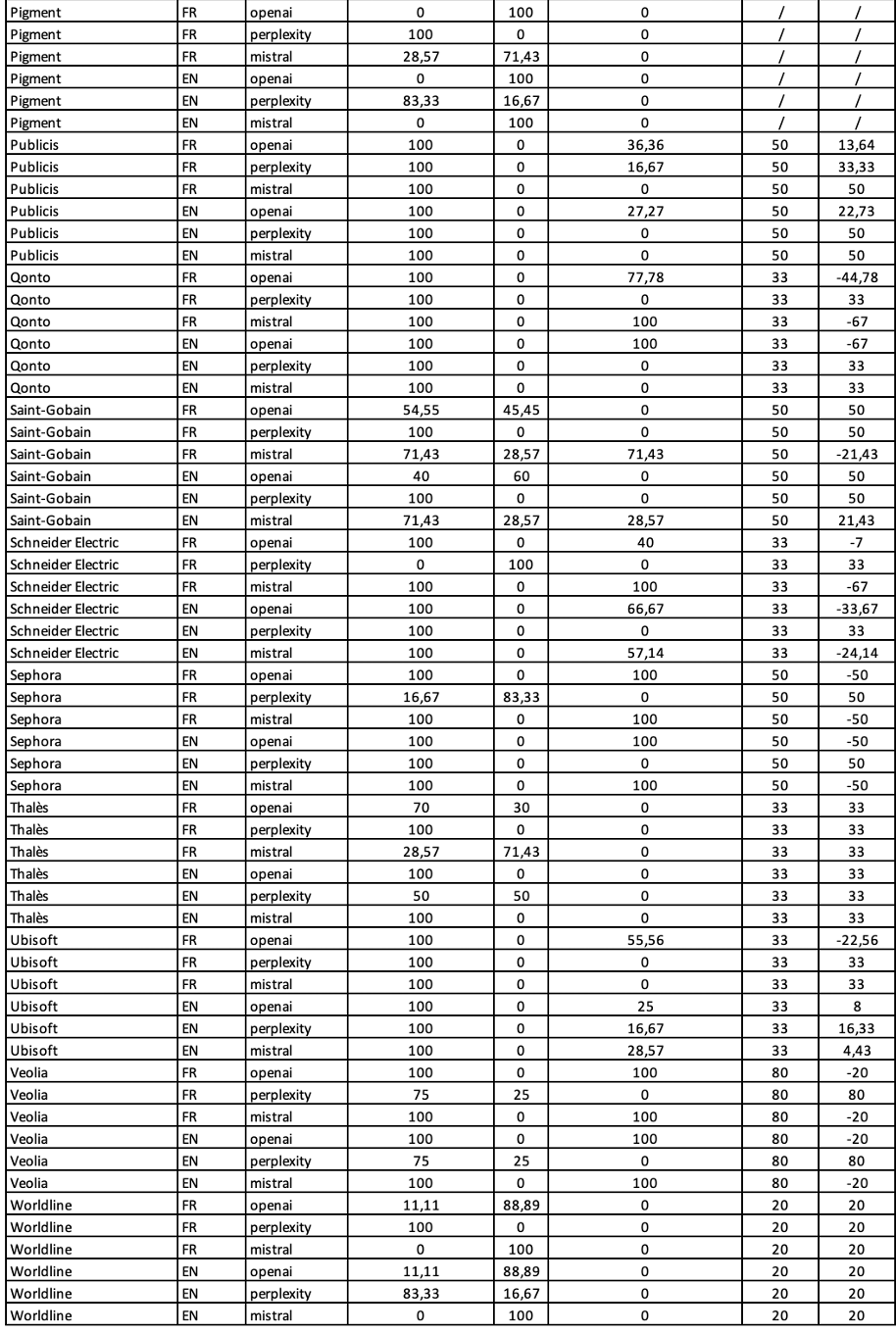

Annex 1: Detailed Results by Company

Annex 2: Methodological Protocol

Collection Period: December 2025

Query Corpus: 857 commercial prompts distributed equally among 20 companies (about 43 queries per company), formulated in French and English. The prompts specifically target the areas of dominance of the tested French companies, justifying that they should in principle be present in all responses.

Sector 1: Industry & Energy

- Schneider Electric

- EN: List the top 5 companies in energy management and building automation

- FR: Liste les 5 meilleures entreprises en gestion d'énergie et automatisation des bâtiments

- Air Liquide (FR)

- EN: List the top 5 global suppliers of industrial gases and hydrogen

- FR: Liste les 5 principaux fournisseurs mondiaux de gaz industriels et d'hydrogène

- Veolia

- EN: List the top 5 companies in environmental solutions (water, waste, energy)

- FR: Liste les 5 entreprises leaders en solutions environnementales (eau, déchets, énergie)

- Saint-Gobain

- EN: List the top 5 manufacturers of sustainable construction materials

- FR: Liste les 5 meilleurs fabricants de matériaux de construction durables

- Thales

- EN: List the top 5 global defense and aerospace electronics contractors

- FR: Liste les 5 principaux contractants mondiaux en électronique de défense et aérospatial

Sector 2: Tech B2B & Software

- Dassault Systèmes

- EN: List the top 5 CAD and PLM software providers for industrial engineering

- FR: Liste les 5 meilleurs logiciels de CAO et PLM pour l'ingénierie industrielle

- Criteo

- EN: List the top 5 advertising platforms for the open internet

- FR: Liste les 5 meilleures plateformes de publicité programmatique pour l'open web

- Dataiku

- EN: List the top 5 enterprise AI platforms for data science collaboration

- FR: Liste les 5 meilleures plateformes d'IA d'entreprise pour la collaboration data

- Pigment

- EN: List the top 5 modern EPM software for financial planning

- FR: Liste les 5 meilleurs logiciels EPM modernes pour la planification financière

- LumApps

- EN: List the top 5 employee experience platforms for internal communication

- FR: List the top 5 employee experience platforms for internal communication

Sector 3: Fintech & Services

- Qonto

- EN: List the top 5 online business banking platforms for European SMEs

- FR: Liste les 5 meilleurs comptes pro en ligne pour les PME européennes

- Worldline

- EN: List the top 5 global payment processing partners for enterprise merchants

- FR: Liste les 5 principaux partenaires de traitement des paiements pour les grands commerçants

- Edenred

- EN: List the top 5 global solutions for employee benefits management

- FR: Liste les 5 meilleures solutions mondiales pour les avantages salariés

- Publicis

- EN: List the top 5 global advertising holding companies by revenue

- FR: Liste les 5 plus grands groupes publicitaires mondiaux par revenus

- AXA (FR)

- EN: List the top 5 global insurance providers for multinational corporations

- FR: Liste les 5 meilleurs assureurs mondiaux pour les grandes entreprises

Sector 4: Consumer & Retail

- Decathlon

- EN: List the top 5 sporting goods retailers with quality private labels

- FR: Liste les 5 meilleurs distributeurs d'articles de sport avec marques propres

- Sephora

- EN: List the top 5 premium beauty retailers with global presence

- FR: Liste les 5 meilleurs distributeurs de produits de beauté premium à présence mondiale

- Ubisoft

- EN: List the top 5 video game publishers for open-world franchises

- FR: Liste les 5 principaux éditeurs de jeux vidéo pour les mondes ouverts

- Accor

- EN: List the top 5 hotel groups for business travelers in Europe and Asia

- FR: Liste les 5 meilleurs groupes hôteliers pour les voyageurs d'affaires en Europe et Asie

- BlaBlaCar

- EN: List the top 5 cost-effective long-distance travel options in Europe

- FR: Liste les 5 options de voyage longue distance les plus économiques en Europe

Models Tested:

- OpenAI GPT-5-mini (version December 2025)

- Perplexity AI Sonar Reasoning Pro (version December 2025)

- Mistral Large Latest (version December 2025)

Experimental Conditions:

- Web search enabled for all models (real-time access)

- Temperature = 1

- No prior context (each query independent)

- Standardized system prompts encouraging exhaustiveness

Calculated Metrics:

- Mention Rate: Proportion of queries where the company appears in the response

- 1st Mention Rate: Proportion of queries where the company is cited in the first position

- AII (Artificial Invisibility Index): 100% - Mention Rate

- ADI (Artificial Downgrade Index): TLS - 1st Mention Rate (where TLS = Theoretical Leadership Share based on market structure)

TLS - Theoretical Leadership Share:

Market Structure Tier Method. It consists of assigning a target score according to the physiognomy of the competition (Duopoly, Oligopoly, or Split Market) and the geographical precision of the prompt.

Here are the 5 tiers used:

- 80% (Undisputed Leader): The company is an undisputed leader and knows no notable similar competitor.

- 50% (The Co-Leader / Dominant): The company is undisputed #1 or #2. It must be cited first one in two times.

- 33% (The Oligopoly - Top 3): The company is part of the global "Big 3" or "Big 4". It must be first one in three times.

- 20% (Competitive Market - Top 5): The sector counts numerous major actors, or the company is a regional leader facing US giants.

- N/A (Invisibility Focus): For challengers, calculating a #1 rank makes no statistical sense. We focus only on their presence (AII).

Group 1: Leader without notable competitor (Target TLS: 80%)

| Company | Justification of TLS 80% |

|---|---|

| Veolia | Since buying Suez, Veolia is the global "Super-Leader" of environmental services, far ahead of Waste Management (very US). |

Group 2: The Dominants & Co-Leaders (Target TLS: 50%)

Expectations are high: they are global giants, often larger than their US competitors.

| Company | Justification of TLS 50% |

|---|---|

| Air Liquide | Quasi-duopolistic market with Linde. Air Liquide is historically and financially the absolute co-leader. |

| Dassault Systèmes | On the specific "Industrial Engineering" segment, CATIA/Solidworks are the global standards against Autodesk/Siemens. |

| Edenred | Undisputed global leader in prepaid service vouchers. WEX is a big competitor but on a different scope. |

| Publicis | With a capitalization having exceeded that of Omnicom and WPP, Publicis has technically become the #1 or #2 in the sector. |

| Saint-Gobain | No US actor has the range width and global footprint of Saint-Gobain on sustainable materials. |

| Sephora | Global icon of selective beauty retail. Ulta is big in the US, but Sephora dominates the "Global Footprint". |

Group 3: The "Top 3" Oligopoly (Target TLS: 33%)

They are indisputable leaders, but face 2 or 3 competitors of equivalent size. Being cited #1 one in three times is the statistical norm.

| Company | Justification of TLS 33% |

|---|---|

| AXA | 1st global insurance brand (Interbrand), but in head-on competition with Ping An (China) and US giants (UnitedHealth/MetLife). |

| Criteo | Open Web Leader, but the "Advertising Platforms" prompt implicitly includes competition with The Trade Desk and Google (DSP). |

| Dataiku | Positioned in the leaders' quadrant (Gartner) facing Databricks and DataRobot. A place in the top three is expected. |

| Decathlon | Unique designer-distributor model. World leader in volume, but facing giants like Dick's (US Retail) or Nike (Direct). |

| Qonto | The prompt specifies "European SMEs". In Europe, Qonto is in the Top 3 of neobanks (with Revolut Business). |

| Schneider Electric | Co-leader with Siemens and Honeywell. |

| Thales | In the global top 3-4 of defense electronics with Raytheon, Lockheed, and BAE Systems. |

| Ubisoft | One of the few publishers capable of releasing AAA "Open Worlds" regularly, facing EA, Take-Two (GTA), and Sony. |

Group 4: Competitive or Regional Markets (Target TLS: 20%)

Very battled or fragmented sectors. Being cited #1 is a performance, but mainly being in the Top 5 is expected.

| Company | Justification of TLS 20% |

|---|---|

| Accor | The prompt targets "Europe & Asia". Accor is very powerful there, but faces the massive striking force of Marriott, Hilton, IHG, and Hyatt. |

| BlaBlaCar | World leader in carpooling, but the prompt is "Economical long-distance travel". It competes with train, bus (FlixBus), and plane. |

| LumApps | "Intranet" Leader, but faces the Microsoft steamroller (SharePoint/Viva) which is often the AI default answer. |

| Worldline | Very fragmented payment market (Fiserv, FIS, Adyen, Stripe, PayPal). Being #1 is hard, but being in the Top 5 is imperative. |

Group 5: The Challenger (Target TLS: N/A)

Here, the objective is visibility (AII), not yet domination (ADI).

| Company | Justification |

|---|---|

| Pigment | Facing Anaplan or Excel, Pigment is a challenger. Calculating a downgrade score (ADI) would be unfair. |

Recognized Methodological Limits: • No American control group (limits France-USA comparison) • Sample limited to 20 companies (partial representativeness) • Temporal snapshot (December 2025) does not capture evolutions • Queries formulated by the Nodiris team (potential formulation bias)

FAQ - Questions about the Study

What is AI invisibility or Artificial Invisibility?

AI invisibility is analyzed in the study using two indicators: the Artificial Invisibility Index (AII) and the Artificial Downgrade Index (ADI). The AII measures the proportion of queries where the company does not appear in the response, while the ADI measures the proportion of queries where the company is not cited in the first position relative to its natural leadership. The study thus reveals that French champions are invisible in 27.19% of queries, and suffer an average downgrade of 16 points.

What is the financial impact of artificial invisibility?

The study concludes that the revenue loss from artificial invisibility is €6 billion in 2026 for the 20 CAC40/Next40 champions analyzed. This figure corresponds to the loss of prospects who turn to AI rather than search engines and no longer see these brands appear. The revenue loss is expected to grow to nearly €10 billion in 2028 when AI represents 50% of internet searches.

Why are French companies more invisible in AI than American companies?

French companies are more invisible in AI than American companies due to a semantic structuring deficit. French companies tend to keep their documentation in closed formats (PDF, Intranet) whereas American giants practice "default to open" and saturate the English-speaking web with structured data that is easy for AI to read.

How can a company improve its visibility in AI?

Companies can improve their visibility in AI by adopting a precise AEO / GEO strategy: structuring their public data, translating their strategic content into English (the dominant language of AI corpora), producing authoritative open-access content, ensuring their content is easy for AI to read and present on authority sources for AI.

A content strategy built for the AI era

Initial diagnostic · First results in weeks